Business

FG Pledges 20-Hour Daily Power Supply to Nigerians by 2027

The Federal Government has set a target to provide Nigerians with a 20-hour daily power supply by 2027, aiming to boost national productivity and quality of life. Learn more about the plans and infrastructure efforts involved.

The Federal Government aims to supply Nigerians with 20 hours of electricity daily by 2027. However, achieving this goal depends on securing sufficient investment in the country’s currently underperforming oil and gas industry, as stated by officials.

Olu Verheijen, serving as the Special Adviser to the President on Energy, announced this during her address at Cape Town’s Energy Week in South Africa. The announcement was relayed by Abiodun Oladunjoye, Director of Information and Publicity for the State House, on Thursday.

“Verheijen disclosed that by 2027, Nigeria plans to provide consumers in urban areas and industrial centers with 20 hours of electricity daily.”

Verheijen’s comments arise amid the ongoing challenges confronting Nigeria’s national power grid, which frequently collapses and causes widespread blackouts. The latest collapse happened on Tuesday, marking the tenth instance in 2024 alone. The Federal Government has identified obsolete infrastructure, inadequate maintenance, and insufficient investment as key reasons for these grid failures.

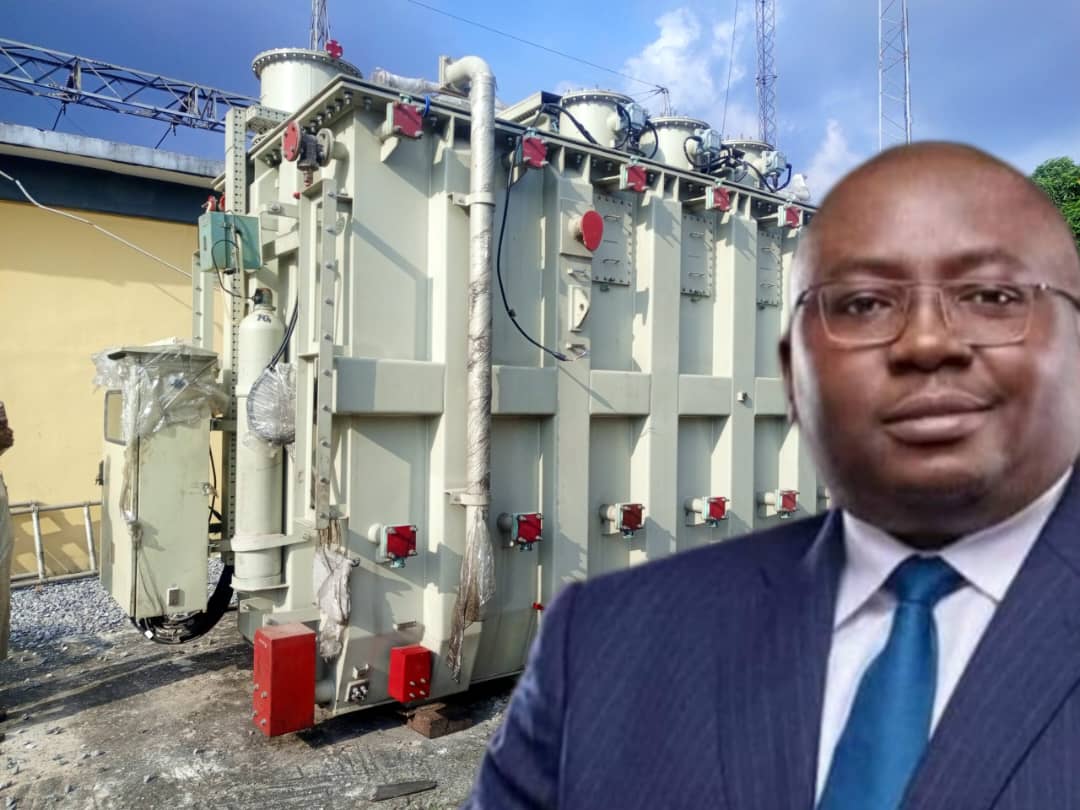

Although Nigeria has an installed generation capacity of approximately 12,500 megawatts, actual production frequently falls short, resulting in unstable power supply for many areas.

During Energy Week, Verheijen emphasized President Bola Tinubu’s administration’s initiatives to overhaul the power sector and provide electricity access to 86 million Nigerians who currently lack reliable energy. She detailed strategies for enhancing revenue collection, minimizing losses by installing seven million smart meters, and expanding off-grid solutions in remote regions.

Verheijen conveyed confidence that Nigeria is on the brink of economic growth, especially after implementing macroeconomic reforms like eliminating the petrol subsidy and liberalizing foreign exchange. “With President Tinubu at the helm, Nigeria is leading efforts to tap into its enormous economic potential and generate employment,” she stated, encouraging international partners to invest in Nigeria’s energy sector.

READ ALSO: Nationwide Power Outage Hits Nigeria as National Grid Fails Yet Again

Verheijen pointed out that Nigeria is underperforming in oil and gas production, even though it has substantial reserves. She highlighted a comparison with Brazil, which possesses only 30% of Nigeria’s oil reserves but produces 131% more oil. “Despite our vast resources, we are not meeting our potential,” she commented. “Brazil manages to produce much more despite having significantly fewer reserves due largely to inadequate investment on our part.”

Since 2016, Nigeria has secured just 4% of the total oil and gas investments made in Africa, with other less resource-rich nations on the continent receiving higher investment levels. Verheijen highlighted that since 2013—when Nigeria’s most recent deepwater project achieved Final Investment Decision (FID)—international oil companies have pledged more than $82 billion to deepwater ventures in other countries.

Recognizing these challenges, Verheijen emphasized President Tinubu’s initiatives to implement reforms designed to revamp Nigeria’s energy sector and draw more investment. She noted the establishment of fiscal incentives specifically for deep offshore and non-associated gas projects—a significant milestone as it marks Nigeria’s first introduction of a dedicated fiscal framework for deepwater gas.

Collaborating with the National Security Adviser’s office, Verheijen’s team has focused on optimizing security protocols in the oil and gas sector. They aim to reduce project durations and operational expenses significantly. “We intend to cut contracting timelines from a lengthy 38 months down to just 135 days,” she stated, “while also working towards removing the current 40 percent cost premium that burdens Nigeria’s petroleum industry.”

The government’s reforms are creating opportunities in the midstream and downstream sectors, encouraging investments in compressed natural gas, liquefied petroleum gas, and electric vehicles. These efforts support the Presidential Gas for Growth Initiative’s broader goals of decreasing reliance on petrol and diesel for heavy transport, decentralized power generation, and cooking.

Verheijen also announced that investments exceeding $1 billion have already been mobilized across Nigeria’s energy value chain, with anticipation of additional significant projects by mid-2025. The government is aiding in the transfer of onshore and shallow water assets to local firms while assisting international oil companies in shifting towards deep offshore ventures and integrated gas projects.

“We have secured over $1 billion in investments throughout the value chain, and by mid-2025, we anticipate reaching a final investment decision on two additional projects. This includes a multibillion-dollar deepwater exploration initiative that will be Nigeria’s first of its kind in more than ten years,” Verheijen concluded.